My conversation with Ludvig Sunström on 25 Minuter: Fabrice Grinda: Angel Investor Extraordinaire and Polymath

By Ludvig Sunström reproduced from StartGainingMomentum

This is a summary of my conversation with Fabrice Grinda for 25 Minuter Podcast, in which we covered topics such as marketplace companies, angel investing, how to know a lot about many things, decision making, self-improvement and book recommendations.

(Be sure to check out the resources in the bottom.)

Highlights / Summary:

Becoming a Polymath:

Having many interests and reading broadly from an early age.

Reading 50-100 books per year.

How does he select new projects to work on?

Mostly by focusing on what is interesting and makes him curious. Years of entrepreneurship and investing have given him Expert Pattern Recognition.

Why are marketplace companies good?

Because they tend towards winner-takes-all, for the category, assuming there is a network effect.

Advice for angel investing:

It is important to specialize and find your niche; but your niche can be broader than commonly assumed. For example, while Fabrice specializes in companies with a marketplace business model, there are many types of marketplace companies (horizontal, verticals, “pick”, B2B) and there are many industries (musical instruments, staples, logistics, food delivery, chemicals, steel, crypto, beauty, etc…) and there are also many different countries. Therefore, he is left with a large range of potential companies to invest in.

What marketplace company would Fabrice start if he were 25-30 years?

Hard to say, because the largest categories have been taken. But as an investor, the most compelling opportunities are currently in the B2B verticals (within a large, fragmented, industry). Good case studies include:

- Flexport (logistics — all industries need it)

- Knowde (matches chemical suppliers)

- Reibus (matches steel supplier)

But these marketplace companies are very hard for a young entrepreneur to start, because it takes a lot of industry expertise and reputation to build them; without that, it’s difficult to get the industry players to join the platform.

The founder of Reibus bought a billion dollars of steel before starting the company. The founder of Knowde came from the industry.

A more general piece of advice would be to look at what the big problems are and how they intersect with your skill set.

9 Macro Factors for 2023-2024:

- Interest rates may go higher and for longer than expected

- The strong dollar is creating a sovereign debt crisis in emerging markets

- There is a new euro crisis looming.

- Real estate prices should continue to fall

- If gas prices go high again, Germany will have a recession

- There is a banking crisis on the horizon

- There is structurally higher geopolitical risk

- Ukraine and Russia will keep grain, gas, and oil prices high

- China is no longer a force for economic growth and disinflation

People are pretty bearish right now, but I think the consensus is wrong in not being bearish enough.

Any one of these nine factors would be enough to create a global recession. What worries me is that most of them are playing out simultaneously suggesting that a replay of the Great Recession of 2007-2008 may be in store.

There is also a massive overhang in Crypto with Genesis, DCG, and possibly Binance.

(Ludvig: My personal belief is that point #1: is especially true.)

But this is good for angel investing

The best investments in the past 10+ years were made around 2008-2009. For the coming decade or so, the equivalent will likely be investments made during Covid 2020 and in 2023-24.

Fabrice’s current portfolio allocation:

20% cash, 70% early-stage tech startups, 10% real estate.

More on Macro: Can the deflationary force of digitization outweigh the inflationary force of higher energy prices?

Not in the short-term. The geopolitical risk is bad. But over the long-run, yes.

Which companies may have increased adoption since Covid?

Food delivery and eCommerce had the biggest boost.

There was a supply crunch, followed by excess demand. Now there is too much competition for a lot of the things that boomed during Covid.

Overall: Very bullish on food delivery (as a category) over the coming 10 years.

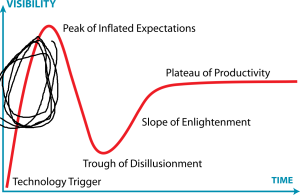

Thoughts on Ai right now?

It appears to be early-to-mid in the Hype Cycle:

I don’t invest in Ai, but the companies I invest in apply it…. I think it [Ai] will become commoditized.

Most likely, the value-added/producer surplus will go to Internet companies. But not necessarily to investors in Ai companies.

Big areas where digitization have yet to have a big impact, but will in another 10 or so years

Public services.

Healthcare.

The education system.

Why are they slow to change?

Due to regulation.

His decision making framework:

Be extremely deliberate about the most important decisions. These type of decisions may only happen once every couple of years. Before making them, consider doing the following:

(1) Write yourself an honest letter/email: What am I happy with? What am I unhappy with? What are all the options, and how can my life be different? (Job, relationship, country). List all available options without limiting yourself.

(2) Share the letter with close friends/advisors: Ask: (a) If it were them, what would they do? (b) Knowing you, if they were you, what would they do?

(3) Try: After getting feedback and ideas, give it a try.

(4) Assess & iterate: What worked? What did not work? Do more of what worked and less of what didn’t.

How to lead an Epic Life:

If you are a knowledge worker, sitting in front of the computer every day, try doing outdoor activities. And if possible, have vacations where you completely disconnect for a week or two, no cell phone, just alone with your thoughts, getting in tune with your intuition.

Vision: 100 years in the future:

- Atomic printer: Giving you all essential things you need (food, clothes, toilet paper, etc)

- You will have more free time

- New status roles will be created

- People will still chase status roles, but a larger percentage of the population will pursue their innate interests

Resources:

Books recommended in the episode:

- A Hero of Two Worlds

- King, Warrior, Magician, Lover

- Project Hail Mary

- More book recommendations (by Fabrice)

Fabrice’s website:

FJ Labs portfolio:

https://fabricegrinda.com/portfolio/

Some great articles of his:

- A Framework for making important decisions (Read all four parts)

- Winter is coming (on macro)

Here are some articles if you want to understand his investing methodology for marketplace companies:

- How FJ Labs evaluates Startups

- Investing in the things that build our world

- All things Marketplaces

- The latest trends in marketplaces (2019 – but still current)

Additional information: On Marketplaces

We do talk quite a bit about marketplace companies (running them and investing in them) but not as much as I had hoped for. Therefore I will share a brief summary below.

The (r)evolutions of marketplace companies:

The Big Bang Beginning: It started with Horizontal marketplaces (having multiple categories by virtue of being first: eBay, Amazon, Craigslist).

(1) Verticalization of marketplaces: After the first ones got all the volume, new companies had to specialize in one niche category. A profitable one. After conquering that category, they can expand TAM by creating additional services for the existing customer base.

(2) Managed marketplaces: “Marketplace pick model” – meaning the marketplace picks the supplier for you. For example, Uber picks a driver nearby you, for you. Provides value for both consumer and service-providers. Consumers don’t have to select the provider, and the service-provider can get more customers (effortless lead-generation, even if the take-rate is high, so most will agree). But this requires a superior matching algorithm. (This is what Fabrice referenced when he said “our companies apply Ai”.)

(3) B2B Marketplaces: Either in a large industry that has been slow to adopt online technology, or in supply chains within a large industry. Online B2B should have happened 10 years ago, it’s just that B2B tends to be family-owned by Boomers, without technological know-how, or there is a strong history and direct relationship between Producer › Reseller › Customer. They could do it more efficiently (cheaper) by skipping the middleman (Reseller) but due to having a many-year long relationship with the Reseller, they won’t do it easily. Overcoming this obstacle requires a better customer experience, and a founder with a strong track-record from the existing industry.

My Final Take on Digitization

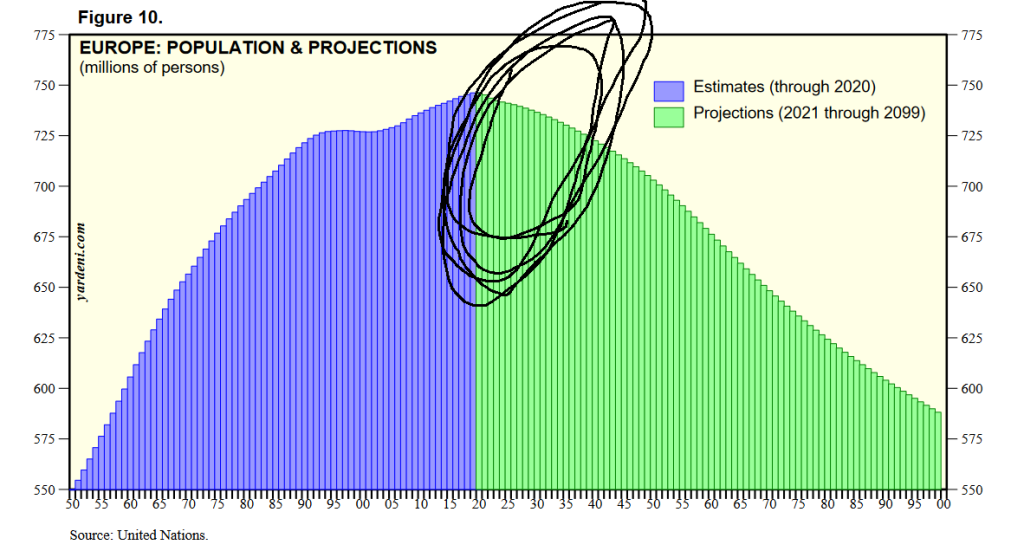

Europe’s population:

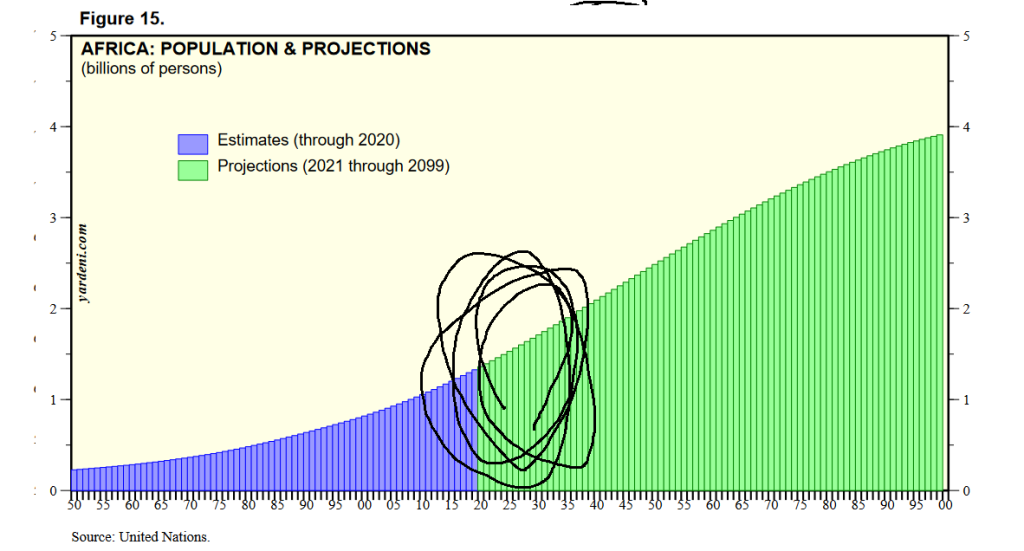

Africa’s population:

Europe’s population is going down.

Africa’s population is going up.

African countries have nowhere near European countries’ spending power, but on the positive side they have fewer established systems (so there is less resistance to behavioral change).

This should increase the total addressable market for all things online and marketplaces, including:

- Online education

- eCommerce

- Digital payments / Crypto

- Online dating

It’s 5-8 years early.

But it will become a tailwind for digitization.

In addition to the embedded podcast player, you can also listen to the podcast on: