I often pondered the makeup of successful founders and founding teams. At FJ Labs we spend a disproportionate amount of time screening for EIRs. We only build 1 or 2 companies per year, so we cannot afford to get it wrong.

I was fascinated to talk Magnus Grimeland and Vegard Medbø of Antler because they filter through 50,000 candidates per year in 30 locations around the world including the US, Europe, Asia, and Africa. Out of the 50,000 candidates, Antler selects 1,500 and ultimately funds around 250 projects.

Potential founders join Antler pre-idea to find potential co-founders and get to an idea. Think of them of the pre-YC YC. Companies coming out of Antler would then be at the stage to go to YC.

Some interesting takeaways from our conversation:

They look for 3 characteristics in founders: spikiness (someone good in something rather than someone well rounded), passion and grit.

It is ok if founders have weaknesses, it is often the flip coin of being spiky and can be compensated with the rest of the team.

You can identify grit in candidates’ backgrounds by making sure they are not jumping around too often and asking the applicants to talk about times when they had staying power in the face of adversity either in a personal or professional context.

The most common mistake they made was overvaluing applicants’ “impressive” backgrounds and resumes.

Their most successful founding teams have 2 or 3 cofounders, but solo founder teams can also succeed.

More than 3 cofounders are not advisable.

Recent trends:

Making work from home less painful

Healthcare

Deep tech

Low code / no code

Continued geographic arbitrage of bringing successful models from one country to another.

If you prefer, you can listen to the episode in the embedded podcast player.

In addition to the above Youtube video and embedded podcast player, you can also listen to the podcast on:

It is extremely hard to succeed as an entrepreneur. Even the most successful entrepreneurs have countless ups and downs. I would argue that I failed my way to success. My brother Olivier, a successful tech entrepreneur and investor in his own right, joins me this week to discuss all the mistakes entrepreneurs make. As we have seemingly made all the mistakes there are to make, we hope you can learn from our mistakes as you go down your entrepreneurial path.

To structure the conversation Olivier prepared a presentation that shows the mistakes entrepreneurs make by funding stage. We share concrete examples from our past with full transparency on metrics and outcomes.

I had a few technical snafus during the first 10 minutes so I apologize for the breaks in the conversation then.

For your reference I am including the slides Olivier used during the episode.

If you prefer, you can listen to the episode in the embedded podcast player.

In addition to the above Youtube video and embedded podcast player, you can also listen to the podcast on:

Early-stage venture capital has undergone a seismic transformation over the past decade as companies stay private longer, raise more capital and exit for larger magnitudes. (NB: the SPAC mania of 2020 may alter this trend, but for now these phenomena still hold). According to SVB, the average VC-backed company at time of IPO in 2018 raised $184M across six rounds, up from $60M across four rounds in 2010. And the average length of time from founding to IPO doubled to 12 years. Meanwhile, valuations have increased accordingly, with 22 $1B+ valuation tech IPOs in 2020 to-date, up from 3 in 2010.

With startups staying private longer and growing larger, Seed and Series A venture investors have come across an interesting dilemma: with limited reserves to follow on across multiple financing rounds, what should they do with their pro ratas in their breakout portfolio companies?

Enter the opportunity fund: a new fund structure soaring in popularity among early-stage GPs that offers an elegant solution to this problem. Done properly, an opportunity fund — sometimes known as a “select fund”, “follow-on fund” or “growth fund” — offers fund limited partners (LPs) the prospect of doubling down on emerging winners in a fund’s portfolio. Per Pitchbook, there have been over 300 “opportunity funds” or “select funds” raised since 2010. However, some LPs have pushed back on this structure, feeling that it serves as an easy way for general partners (GPs) to gather AUM and a distraction from their job of managing a Seed-stage portfolio.

At FJ Labs, we currently angel invest from one fund across different stages, and we have been studying whether it makes sense to silo our investments into an early stage (Pre-Seed-A fund) fund and a Growth/opportunity fund. My research partner Luke and I were shocked by the dearth of available literature on the subject; virtually no one has published any articles or papers on opportunity funds, perhaps because of how new they are. So we embarked on a journey to interview some of the premier early-stage fund managers who have pioneered these vehicles and the LPs who evaluate and invest in them. We surveyed over 30 venture capital managers ranging from Seed stage to pre-IPO, and LPs ranging from family offices to fund of funds to state retirement plans. We left with a thorough understanding of best practices in structuring growth/opportunity funds and reached a high-conviction conclusion for how we should structure our next fund(s).

Methodology

We approached this like a research project. We began by reading ~50 blogs, academic papers & research articles. We made it a point to understand divergent schools of thought regarding portfolio construction — spray and pray, algorithmic, concentrated — because it helps underscore why VCs and LPs alike have focused their energy on opportunity funds. Our reading ranged from early-stage investment best practices to Abe Othman’s amazing posts using AngelList data to growth equity best practices. This research culminated in an understanding of who we wanted to interview and what questions we would need to have answered.

We laid a foundation by benchmarking fees and returns and layered on an understanding of follow-on investments, conflicts of interest, and capital allocation. Next, we dove into why firms created their opportunity funds, how LPs viewed them, and how they’ve performed.

Finally, we created a functional fund model, utilizing FJ’s current portfolio to inform it. We’ll share a more simplified and generalized model, below.

General Context

So, what are GPs and LPs saying about opportunity funds more broadly? We’ve gathered a select handful of quotes to set the stage…

“LPs don’t love opportunity funds. They want true seed risk.” — GP

“We are more time-constrained than cash-constrained. We can’t invest in 2x the number of companies, so this is a way to cram more dollars in companies we’re excited about.” — GP

“Generally speaking, we try not to do opportunity funds.” — LP

“Some opportunity funds have outperformed their core funds!” — LP

Findings

Portfolio Construction

“Most opportunity funds are more concentrated because you’ve had a filter or two against the investment set.” — LP

While there are differing opinions on optimal portfolio construction at the early and growth stage, there is consensus that opportunity funds should consist of six to ten unique positions. The number of investments is informed by the number of prior investments across funds for each GP. In other words, an opportunity fund is a mechanism for GPs to double down on the top 5% of their investments. Likewise, LPs obtain access to the best investment opportunities and benefit from their GPs’ insider information on their portfolios.

Why not raise a bigger fund?

Separate funds enable GPs to write larger checks in their emerging, later-stage winners without diluting their early stage portfolio. However, writing large checks from one fund may lead to LP concerns regarding style drift (“We invested in you as a Seed fund manager”). Providing LPs with two tightly-defined products with specific risk/reward profiles can more effectively cater to their needs.

Additionally, some LPs can’t evaluate individual co-investment opportunities and would prefer to participate in a “best of” style opportunity fund. In effect, LPs get access to all follow-ons, rather than select investments via SPVs, and from a GP perspective, this is far more convenient to administer than ad hoc SPVs.

While there is precedent for Seed-to-IPO funds like Insight Partners and NEA, trying to expand beyond the early stage requires a change in firm strategy. This is not the case with opportunity funds, which are typically more passive, follow-on vehicles (as we’ll discuss below, opportunity funds should not lead, running counter to multi-stage fund strategy). If you plan to remain an early-stage investor, the opportunity fund is the right vehicle for you to double down on winners. If you want to create a franchise that invests across all stages, then it makes sense to explore a multi-stage fund.

Fund Economics

“We invest for 20% IRR regardless of the asset class. A good opportunity fund is 2X net, 20% IRR. — LP

“If you can return 2X net to your LPs w/ 20% gross IRRs, you can raise capital forever” — GP

Our survey confirmed that venture investors and LPs target a 3X net fund return across early-stage, growth stage, and opportunity funds. However, we also learned that if VCs can achieve at least 2X MOIC returns or 20%+ IRRs, they will be able to keep raising funds for years to come. Opportunity funds are measured against the same benchmarks. However, given how new these vehicles are, we don’t have comprehensive data on their performance.

While return expectations are the same, fee structure differs by fund type. We did not come to a consensus on fees and carry for opportunity funds. That said, there is agreement that whatever your fees and carry on your early-stage fund, you should take less on the opportunity fund. Otherwise, LPs will feel that you are taking advantage of a new vehicle to increase AUM. Perhaps this is why it is seen as best practice for GPs to only take fees on invested capital from the opportunity fund (vs. on committed capital for traditional funds).

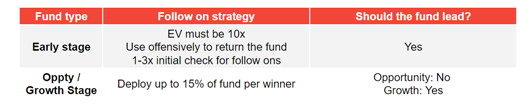

Follow-ons and Leading

“Only invest in companies that are outside-led growth rounds that are growing 2X a year.” — Opportunity fund GP

“If I could go back to the beginning of my career, I’d say the one thing to know is the magnitude of exit will get bigger by another standard deviation.” — LP

Follow on strategy begins with doubling down on winners. Best practice indicates that GPs should not use opportunity funds to protect existing investments, should not lead investment rounds with their opportunity funds, and should create systematic rules for which fund (early-stage vs. opportunity) gets pro rata rights.

Most commonly, use of pro rata rights is separated by investment stage. For example, an early-stage fund may invest until Series B, at which point an opportunity fund invests in Series C+. This cutoff can be delineated by round size, valuation, or some combination. It is wise to have clearly defined rules around selling secondaries, down rounds/pay to play mechanisms, bridge rounds, incubator/accelerator companies (if your firm has one), etc. Often, managers will consult with their Limited Partner Advisory Committees (LPAC) for edge cases or complex scenarios.

LP Preferences

“Managers often ‘staple’ funds together: if you want access to a Seed fund, you have to invest a ratable amount in that manager’s opportunity fund. However, it is important for VCs to only do this practice with new LPs.” — GP

“Ultimately, a lot of these get raised on how sexy the GP is.” — LP

We found that LPs don’t like being stapled but often don’t mind insomuch as they are granted early-stage fund exposure. Some firms use formulas to give larger / more loyal LPs higher allocations in early-stage funds. Interestingly, while LPs are thought to hate opportunity funds, we did not observe overwhelming distaste for them among our interviewees. Rather, we found that the jury is still out until we can see widespread data from the past ten years.

Nor did we come to a firm conclusion if LPs preferred individual co-investment opportunities versus an opportunity fund that aggregates them. Some more nimble LPs such as family offices like to participate in direct co-invests, while other, slower-moving institutions prefer for the manager to do by follow-on investing via an opportunity fund.

Additionally, LPs had differing opinions on participation in opportunity funds, depending on the risk/reward profile they were looking for. Institutional LPs will typically view opportunity funds more favorably, as will any LPs looking for a shorter time to liquidity.

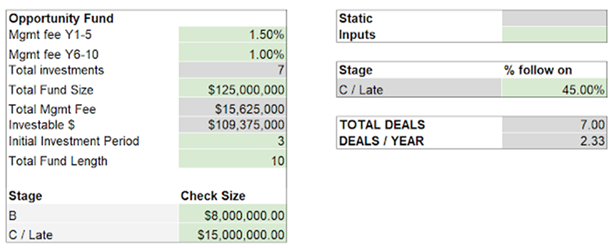

Fund Model

We mentioned earlier that the opportunity fund model is informed by prior fund construction. We simplified and generalized our model to demonstrate this:

In this case, we wanted to end up with an opportunity fund that supports two 30-company early-stage funds. Assuming that the top 10% of companies across these funds will be breakouts, that implies a portfolio of ~6 companies. You can adjust the inputs to tailor the fund construction given your portfolio makeup and investment pace. You can also back into the correct check sizes (for each stage) by examining your pro-rata rights and ownership across the portfolio. You should raise this fund with certain portfolio company high-flyers in mind, but do not advertise your fund as if you will have guaranteed allocation.

Conclusions

Opportunity Funds allow LPs to titrate their risk exposure and for GPs to provide more tightly-defined products to effectively cater to their investors’ needs. They are easier to administer and capture more value than ad hoc SPVs, which run a higher risk of losing LP capital and have to be spun up one-by-one. If investors separate funds, they can write large checks at later stages without diluting their early-stage investments.

Opportunity fund LPs are typically satisfied with returns of 2X Net MOIC and 20% IRR. Opportunity funds typically focus on existing portfolio companies and are run by existing investors, whereas growth funds are typically run by separate teams and focus on new investments. There is an expectation that opportunity funds carry lower fees and run a more concentrated portfolio than early-stage funds.

Unfortunately, there is not enough public data to evaluate their returns to-date, but judging from their proliferation and the expansion of venture capital as an asset class, we suspect opportunity funds are here to stay.

—

Jeff Weinstein is a Principal at FJ Labs, an early-stage venture fund and startup studio that invests in and builds online marketplaces. Jeff co-heads the fund’s 500+ investments which have included Alibaba, Flexport, Rappi, Betterment, Fanduel and Delivery Hero, and also manages FJ’s external fundraising efforts. Jeff was previously a Senior Associate at Lux Capital, and prior to that worked at a fund of hedge funds. Jeff is in Class 24 of the Kauffman Fellows.

Luke is an MBA candidate at the University of Chicago Booth School of Business with concentrations in Finance, Entrepreneurship, and Strategic Management. In addition to his work with Jeff at FJ Labs, Luke is an Associate at M25 in Chicago, where he focuses on investing in early-stage startups. He previously worked as a Product Manager at three B2B tech start-ups in Chicago, spanning the benefits administration, fintech and human capital management spaces.

Christian is the rare breed of polymath Renaissance Man operating in a world that rewards specialization. We had an extremely broad and far-ranging conversation covering:

Whether you should always pursue your passion

The relative importance of focus

How to make the most of the opportunities presented to you

Spirituality

Happiness

Psychedelics: why they are improperly maligned, our respective journeys, and how he turned a moment of self-discovery into a billion-dollar business

The latest findings on longevity and metformin

The importance of sleep

The role of Bitcoin as a store of value in a world of increasing asset prices driven by low interest rates

His involvement in film and desire to create optimistic stories

How to reinvigorate the West and competition with China

Christian’s two must-read books

Three technology trends we are excited about in the coming decade

If you prefer, you can listen to the episode in the embedded podcast player.

In addition to the above Youtube video and embedded podcast player, you can also listen to the podcast on:

The best-laid plans of mice and men often go awry. As you may recall, I ended 2019 intent on selling my New York apartment and renting an apartment March 2020 onwards. The idea was to live a hybrid life where I split my time between New York and Turks & Caicos.

I wanted to spend every other month in New York intellectually, socially, professionally and artistically stimulated beyond my wildest dreams, meeting countless extraordinary people, hosting intellectual dialoging salons and enjoying all of New York’s entertainment options. Then I wanted to head to Turks & Caicos to work during the day, kite, and play tennis, and really take the time to read, be reflective and recharge my batteries.

As you might suspect, the year played out rather differently. The year started out as expected. I went heliskiing in Canada. I went to the fantastic Upfront Summit in LA. I hosted FJ Labs’ bi-annual brainstorming retreat at my place in Turks & Caicos. I went to check out the gorgeous Sanctuary in Utah. I had been inspired by their manifesto and jumped at the opportunity to experience it firsthand. I love their vision and they built the most beautiful contemporary chalets I have ever seen. However, it helped me realize that ultimately Revelstoke in Canada pulls at my heart strings and would make a better winter base as the mecca of extreme winter sports with its renowned steep and deep tree skiing. Not that I have decided to implement that vision yet, but it is nice to dream.

As February wore on, I started pondering the potential impact of COVID-19. I wrote an article in February suggesting COVID-19 could be the black swan causing the next global recession. I sent a message to my friends in early March telling them that staying in a high-density city like New York during a pandemic made no sense. I invited them to join me in Turks & Caicos. Eleven of them responded to the call. We became a pandemic family.

We were quite the motley crew as we were the random assortment of the first eleven people who decided to join me. I had distributed the invitation widely so many of us did not know each other that well before quarantine. We were all in different stages of life including 4 kids ages 12 through 14.

Despite being the most unexpected of groups, I could not have hoped for a better outcome. We all took turns doing tasks in the house and brought our varied skills, passions and energies to bear. We also realized how privileged we were to both have each other at a moment during which many were isolated and alone, and to have the opportunity to enjoy the outdoors and practice sports or find alone time when most could not leave their homes.

It was a really nice change of pace not to travel for five and a half months and lead a more domestic existence. Like most people, I typically only do important or urgent things on my to do list, but rarely get to the “nice to do”. With urban life on hold, I took advantage of the opportunity to tackle those. I redesigned my blog. I redid the website of my villa in Turks and took control of its marketing such that most rentals now come directly rather than through Luxury Retreats. I started a live streaming show, Playing With Unicorns, to share everything I wish I knew when I started out as an entrepreneur. I read and wrote more than ever before. I improved at kiting. I built the first padel court in Turks and Caicos and spent countless hours practicing.

Come late August, I was itching for a change. I decided to go camping in Yellowstone. It was a fun weeklong trip off grid with no cell reception where you carry everything you need including your tent, sleeping bag and food in your bag pack as you go from camp site to camp site. It was gorgeous and refreshing. A freak August snowstorm reminded me that the best stories are born of adversity. It was a great complement for a trip to the Aman in Jackson Hole.

In the fall, I also went camping on Governor’s Island, went to see the foliage change in Lake Placid, and reconnected with the FJ Labs team in New York.

I was also able to bring my extended family together for the holidays. It is something my grandmother Francoise used to do yearly. However, it is a family tradition that had dissipated since she passed. With the help of my cousin Nalle, I was delighted to be able to restart the tradition. We were especially lucky to be able to get together in Covid times when many are separated from their families. We all got PCR tested before spending 19 days together in Turks & Caicos and were able to stay safe while having an amazing time. I was elated to be able to spend time with my parents, cousins, brothers and uncle for the first time in over a year!

FJ Labs continued to rock. 2020 was our most prolific year ever. The team grew to 28 people. We deployed $57M. We made 146 investments, 97 first time investments and 49 follow-on investments. We had 27 exits, of which 15 were successful including the IPOs of Wish and Airbnb, the IPO of OpenDoor via SPAC, the IPOs of Meliuz and Enjoei on Brazil’s B3 exchange, the acquisition of Postmates by Uber and the acquisition of Fanduel by Flutter Entertainment.

Since Jose and I started angel investing 22 years ago, we invested in 655 unique companies, had 218 exits (including partial exits where we more than recouped our cost basis), and currently have 603 active investments. We had realized returns of 61% IRR and a 4.8x average multiple. In total we deployed $320M of which $120M was provided by Jose and me.

I came to realize that my willingness to participate in panels or give keynote speeches grows dramatically if I do not need to travel for them and I gave more speeches and appeared on more podcasts than ever before. To avoid redundancy, I tried to cover different topics and content and ultimately used a lot of this content for various Playing with Unicorns episodes including FJ Labs’ Investment Thesis and FJ Labs’ Startup Studio Model.

The keynote I am most proud of and did the most research on is my case for technology-led optimism despite the pandemic, populism, climate change, policy failure, social unrest and social injustice. It is worth watching in full and I am including the slides below for your reference.

Most of my writing was professional in nature this year largely driven by all the content I needed to create for Playing With Unicorns. My best blog posts were:

I continued to be a very prolific reader in 2020. It is probably worth mentioning that most of what I read is fiction and most of that is science fiction though I dabble in every genre. My favorite non-fiction books of 2020 were:

In general, I do not read “business books” as I find them simplistic. Loonshots is the exception to that rule. It blew me away. It mixes compelling personal narratives of entrepreneurs like Edwin Land (Polaroid) and Juan Trippe (Pan Am) with observations from physics and history to weave a very compelling narrative. I also had the pleasure of having its author, Safi Bahcall, on Playing With Unicorns for a fun and wide ranging conversation.

From a macroeconomic perspective, COVID-19 brought the longest expansion on record to a screeching halt with the lockdown leading to levels of unemployment and economic contraction not seen since the Great Depression. As I predicted, the second order economic impact of the pandemic was more damaging than the first order costs of treating infected people or lost wages from people not working because they are sick. Also as predicted, governments and central banks threw everything including the kitchen sink at this problem.

Given the curtailing of economic activity due to restrictions, the greater short-term risk is deflationary. In the near term historically low interest rates are making the record levels of debt manageable. However, the massive debt overhang will require delicate macroeconomic management to avoid a massive financial crisis.

Record low interest rates are also fueling asset price inflation across most asset classes and a full-on bubble in SPACs. Outside of commercial and residential real estate in major cities, it feels like we are in the late stages of a low interest rate fueled “everything bubble” with extreme frothiness across most asset classes. It may very well continue for a while as there is increasing optimism about the end of the pandemic. However, at some point the harsh reality of weak underlying economic conditions may very well temper today’s frothiness and excessive valuations. I will not be so foolish as to pretend I can predict when the bubble will pop, but I would not be surprised if it happened in 2021.

Historically crisis have accelerated underlying trends and been a source of innovation. The 1930s saw the greatest increase in productivity growth in the US as necessity is the mother of invention. Likewise, the most defining companies of the last decade, Airbnb, Cloudflare, Github, Pinterest, Slack, Square, Stripe, Uber and Whatsapp, were founded during the financial crisis of 2008-2009. Uber and Airbnb grew dramatically as individuals’ personal financial difficulties led them to consider renting their apartment to strangers or becoming part time drivers for the first time.

The most interesting companies of the coming decade will likely have been created or come of age in COVID times. This past year has seen a rapid increase in online adoption across most categories. Some sectors such as online food and grocery delivery, telemedicine, online education, and remote work exploded, while others such as ecommerce, online gaming and video grew significantly from already large bases.

Given that online experiences are more convenient and less expensive than the alternative, this increase is here to stay. While some sectors might give back a bit of the growth, in general, there has been a step change in penetration, and they will grow from this increased base.

I am extremely grateful for the year I had, surrounded by loved ones in a safe place and privileged to be able to work remotely in a sector that has benefited from COVID. I am excited that human ingenuity led to the creation of a new class of vaccines in record time. I am hopeful that by the second half of the year we will be able to return to a semblance of normality and put an end to the personal and economic suffering this crisis has caused.